Global markets finished the week higher

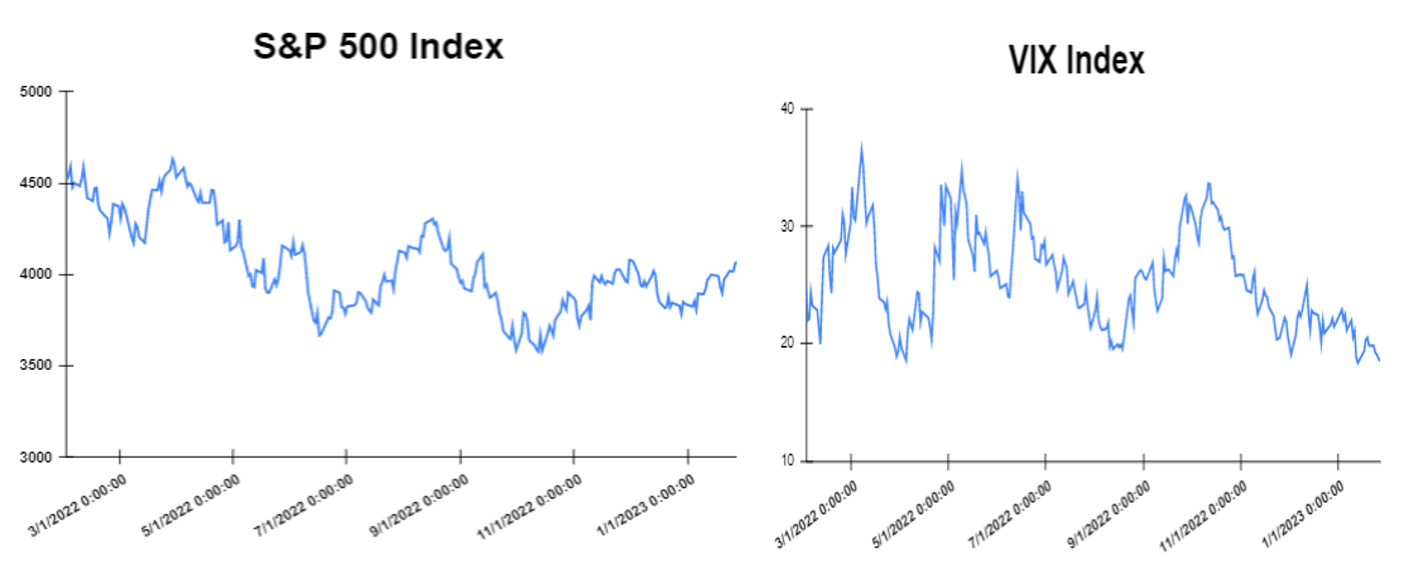

Global markets started the week higher. Consumer confidence in the euro area improved in January compared to the previous month. According to the report, the recovery is reflected in an increase of 1.4 percentage points in the EU and 1.1 percentage points in the eurozone. In addition the eurozone flash PMI unexpectedly moved back into expansionary territory as it came in at 50.2 in January, up from 49.3 in December. Moreover, on Thursday markets rose on surprisingly good GDP growth. Specifically, the gross domestic product (GDP) of the United States grew by 2.9% in the fourth quarter of 2022 compared to the same period in the previous year, which it was better than expected. Lastly, the Personal consumption expenditures (PCE), excluding food and energy, increased by 4.4% from a year ago, down from the 4.7% reading in November. This was in line with expectations and showed further easing in inflationary pressures. Also, that was the slowest annual rate of increase since October 2021. The Dow Jones gained 0.008% at the closing bell on Friday. The S&P 500 increased by 0.25%. Furthermore, the DAX, CAC 40 and the FTSE 100 were flat at the closing. In addition, investors are looking forward to the inflation data in Europe on Wednesday.

Treasury yields advanced towards the end of the week

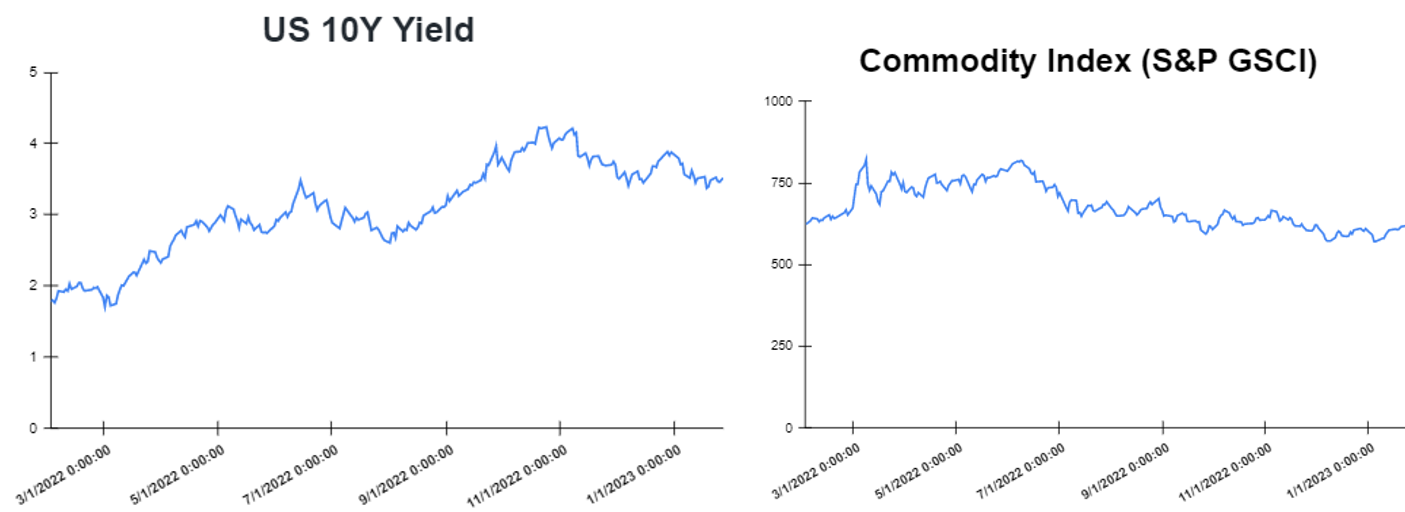

Yields advanced after a key inflation report watched by the Federal Reserve indicated a sizable increase in prices. The core personal consumption price expenditures index rose by 4.4% from a year ago in December, the Commerce Department reported Friday. That was in line with economists’ consensus estimate from Dow Jones. Including food and energy costs, inflation was up by 5% on an annual basis. The yield on the 2-year Treasury increased to 4.205%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.515%, up by about 2 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.6360%. The spread between the US 2’s and 10’s tightened to -69bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) widened to – 125.6bps. Meanwhile, investors are looking to the next Fed Interest Rate Decision on Wednesday, which is expected to grow to 4.75% from the previous 4.50%.

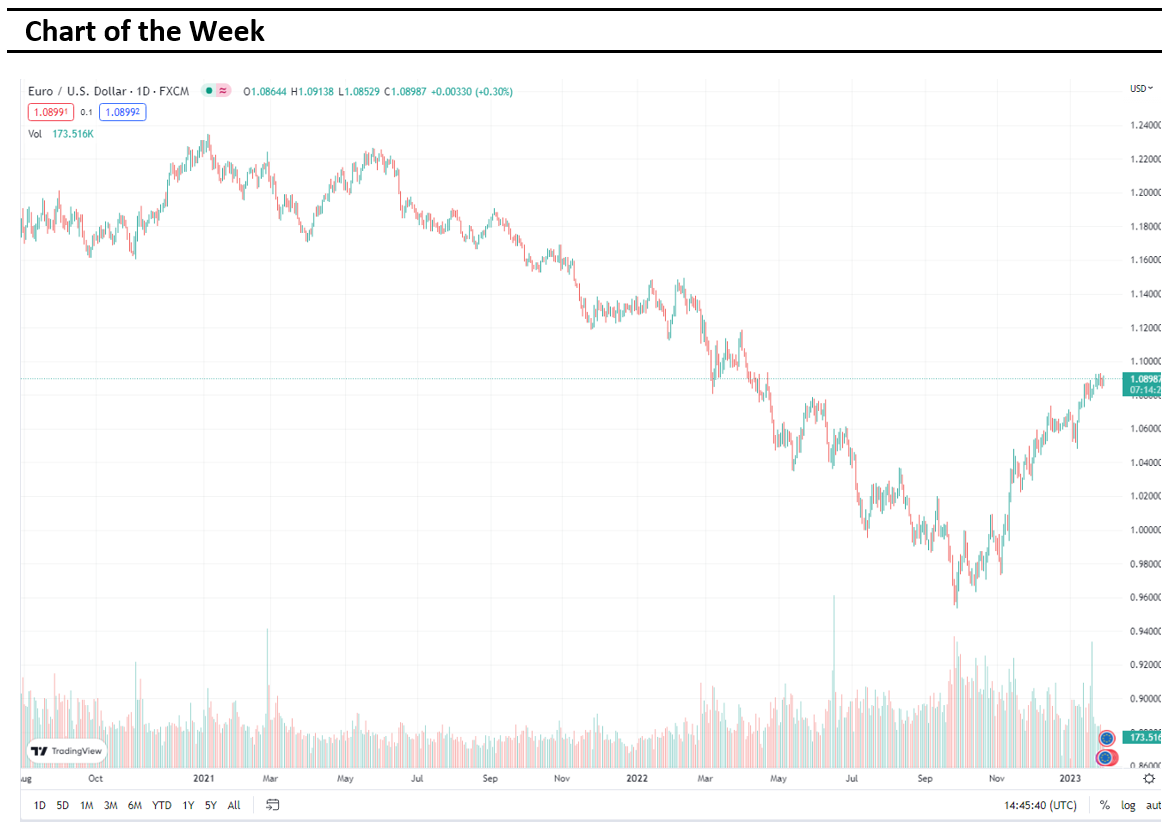

Volatile week for USD

The US Dollar moved higher towards the end of the week after Gross Domestic Product increased at a faster-than-expected 2.9% annual rate in the fourth quarter of last year as consumers boosted spending on goods. In addition, Inflation data also gave rise to prospects of dovish Fed with Personal Consumption Expenditures growth slowed to 2.1% year over year from 2.3%. Therefore, the EURUSD traded lower at 1.08725. Furthermore, the GBPUSD ended the week lower at 1.2397 and the USDJPY traded lower at 129.89 on Friday. Adding up, investors are looking forward to the interest rates of ECB, BOE and US fed, due to be released on Wednesday and Thursday.

Oil and Gold traded lower towards the end of the week

Gold started the week lower after concerns over interest rates increases. However, Gold traded higher in the middle of the week as the dollar weakened and investors kept a close eye on a slew of upcoming U.S. economic data. Gold traded lower at the end of the week after a recovery in the dollar following a better-than-expected US economic growth figures. Prices of Oil moved higher at the start of the week, after further curbs on Russian oil looming as the West agreed to review the price ceiling levels again in March. However, on Friday, the prices of oil futures sank as investors awaited Baker Hughes’ rig count weekly report. Meanwhile, the Crude Oil Inventories report will be released on Wednesday.

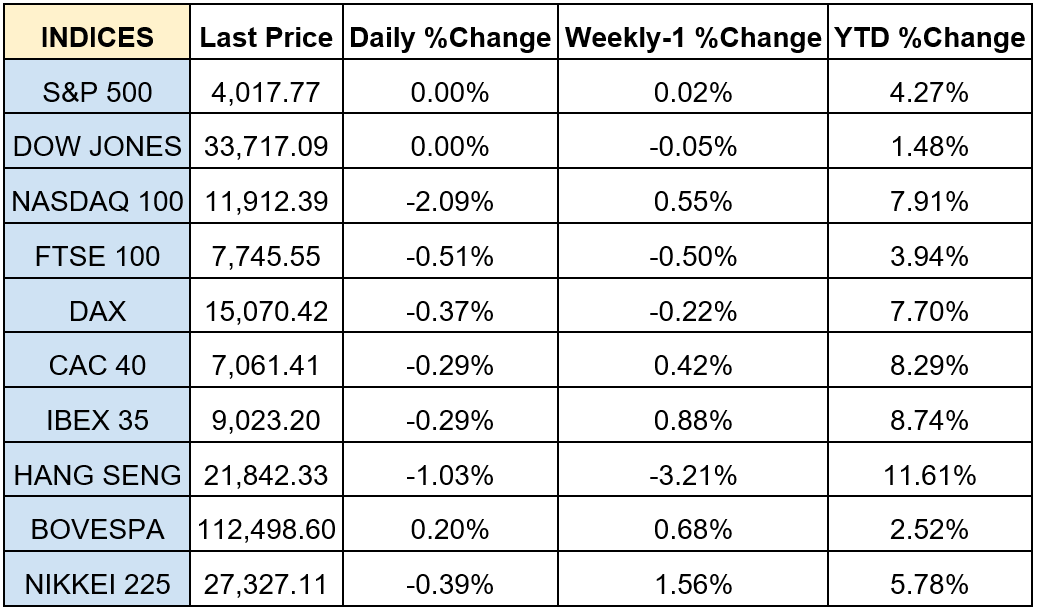

Stock indices performance

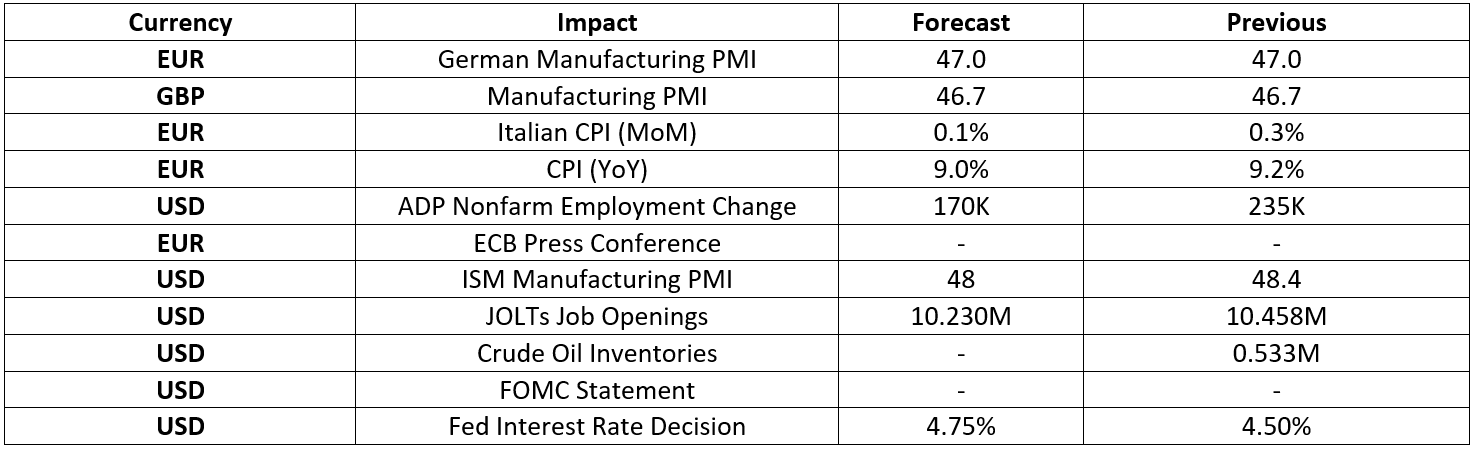

Key weekly events:

Monday- 30 January 2023

Tuesday – 31 January 2023

Wednesday – 01 February 2023

Thursday – 02 February 2023

Friday – 03 February 2023

Sources: