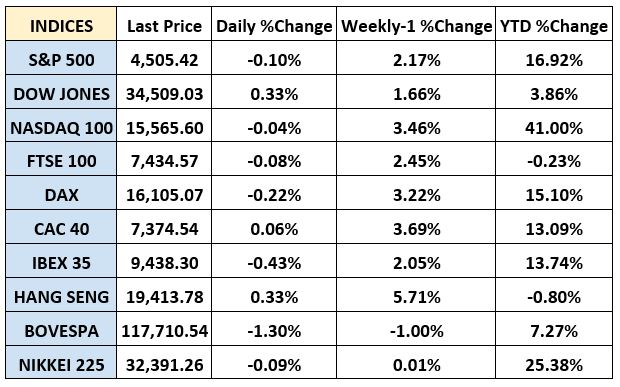

Global markets finished the week mixed

The global markets started the week higher as investors are waiting for the incoming economic data. On Tuesday, the unemployment rate in the United Kingdom clocked in at 4% in May, going up 0.2 percentage points in comparison to the previous month. On Wednesday, Global markets closed sharply higher as the annual inflation in the United States stood at 3.0% in June, going down from the4.0% registered in May and coming in slightly lower than analysts forecast. On Thursday, the gross domestic product (GDP) of the United Kingdom shrank by0.1% in May compared to the previous month. On the same day, the Producer Price Index (PPI) for final demand in the United States increased by 0.1% in June compared to the previous month. Following the above news, the Global market closed with strong gains on Thursday. On Friday the Global markets closed mixed as investors are waiting for the new economic data including those on the Eurozone and the United Kingdom’s inflation and Germany’s producer prices. Moreover, on the same day, the Consumer Sentiment Index in the United States observed a monthly rise of 12.7% in July hitting 72.6 points, its highest level since September 2021. The Dow Jones closed with a gain of 0.33% at the closing bell on Friday. The S&P fell by 0.10%. Furthermore, the DAX declined by 0.22% and the CAC 40 jumped by 0.13%. The FTSE 100 stood flat.

Treasury yields were advanced towards the end of the week

Yields were higher at the start of the week as investors awaited the latest comments from U.S. Federal Reserve officials and key inflation data due this week. However, yields moved lower on Wednesday after the inflation report in June showed an easing in prices. The consumer price index increased by 3% from a year ago, which is the lowest level since March 2021. On Friday, yields closed the week higher reversing some of the sharpest declines seen over the last two sessions on the back of cooler-than-expected consumer and wholesale inflation prints. Specifically, on Friday, the yield on the 2-year Treasury decreased to 4.738%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.811%, growing by about 5 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.9240%. The spread between the US 2’s and 10’s advanced to -92.7bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) advanced to – 135.4 bps

In addition, investors are looking forward to the Europe and Great Britain inflation (CPI) data expecting a decrease

Volatile week for USD

The US Dollar at the start of the week was lower affected by data reflecting lower inflation expectations and on the back of a decline in US Treasury yields. In the middle of the week the US Dollar declined as inflation data from the US led to sharp market moves. However, on Friday, the US dollar finished lower suffering its worst weekly loss since November of last year, falling below 100.00, to the lowest since April 2022. The Greenback remains vulnerable in the context of risk appetite and lower Treasury yields. The EURUSD increased to 1.18, while the GBPUSD increased to 1.31. Additionally, the USDJPY decreased to 137 Yen on Friday.

Oil and Gold traded mixed towards the end of the week

Gold started the week higher as investors were shifting their focus towards the United States Consumer Price Index (CPI) after the impact of the Nonfarm Payrolls (NFP) report. However, Gold traded higher at the end of the week sticking to near one-month highs as softer-than-expected U.S. inflation data saw investors reassess just how much further U.S. interest rates will rise. On the other hand, oil prices decreased on Monday after the newest report on China’s annual inflation in June showed no change compared to the previous month. However, oil finished lower at the end of the week, as the dollar strengthened and oil traders booked profits from a strong rally, with crude benchmarks recording their third-straight weekly gain. Meanwhile, Russia reiterated its intention to reduce its output by 500,000 barrels per day (bpd) in August by delivering fewer exports. Meanwhile, the Crude Oil Inventories report will be released on Wednesday which is expected to show a decrease of 6.851M.

Stock indices performance

Key weekly events:

Tuesday – 18 July 2023

Wednesday – 19 July 2023

Thursday – 20 July 2023

Friday – 21 July 2023

Sources:

https://www.tradingview.com/

https://breakingthenews.net/Home

https://www.investing.com/

https://www.fxstreet.com/news

https://www.cnbc.com/world/